Dear investors,

The first half of the year saw a continuation of the stock market rally that began almost 3 years ago, against a very active political and geopolitical backdrop. The period was very favourable for the ‘momentum’ style, reflecting the strong trends seen in the market. At the end of June, the MSCI Europe NR posted a +8.5% return in EUR since the start of the year, and the MSCI USA NR +6.1% in USD.

Against this backdrop, all European Digital Stars strategies outperformed over the year, benefiting from sustainable trends in several market segments that had been identified in advance, particularly in the defence and finance sectors.

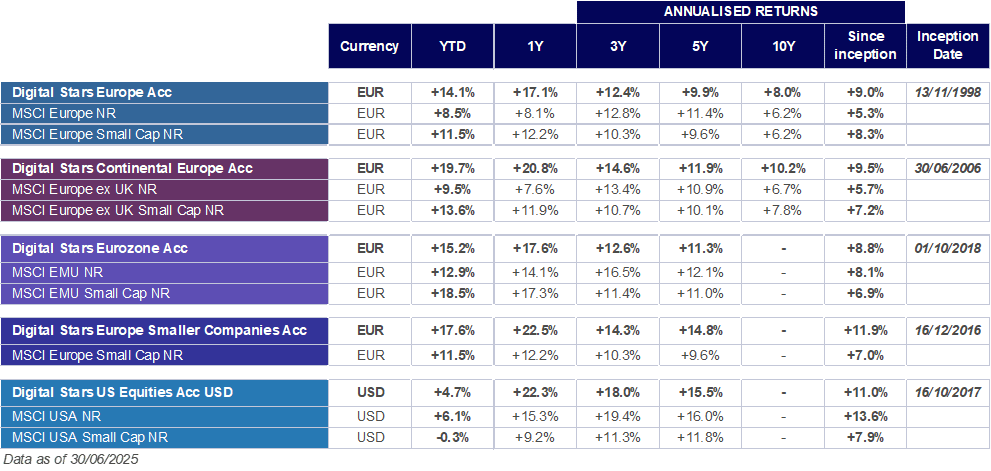

Annualised performance of Digital Stars funds

Risk indicator: 5/7

Source: FactSet/Chahine. Data as of 30/06/2025. Past performance is not indicative of future returns.

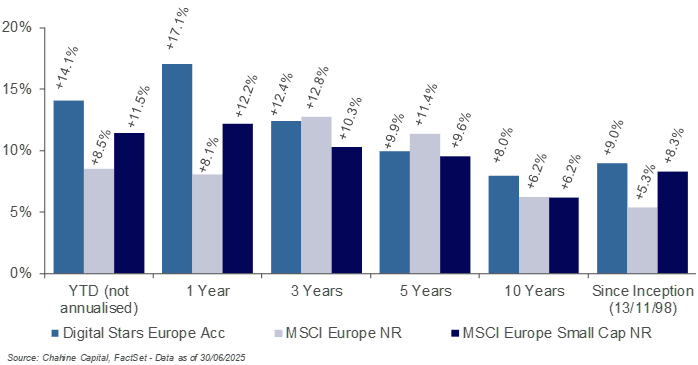

Digital Stars Europe (retail share class)

Source: FactSet/Chahine. Data as of 30/06/2025. Past performance is not indicative of future returns.

Over the first half of 2025, the fund’s “pro-cyclical” positioning has been favourable for Digital Stars Europe, particularly since the beginning of March when the small- and mid-caps began their rebound relative to the market. The wide dispersion within European equities has supported good stock selection, with a clear focus on the market’s strongest trends. The fund benefited from excellent sector positioning, with an overweight in financials and industrials, two of the market’s leading sectors in terms of weight and performance, and a clear underweight in healthcare and consumer staples. In the end, the fund benefited from the value theme and the renewed interest in defence.

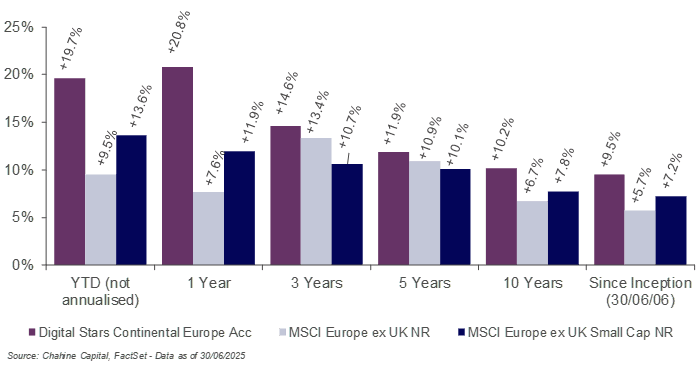

Digital Stars Continental Europe (retail share class)

Source: FactSet/Chahine. Data as of 30/06/2025. Past performance is not indicative of future returns.

In the first half of 2025, Digital Stars Continental Europe benefited from its “pro-cyclical” all-cap positioning, as well as from a good selection of stocks, supported by a positioning well oriented towards strong underlying market trends. The fund’s overweighting of financials and industrials, and underweighting of healthcare, consumer discretionary (particularly luxury goods) and technology, contributed positively to the fund’s outperformance, echoing a favourable year for value and defence.

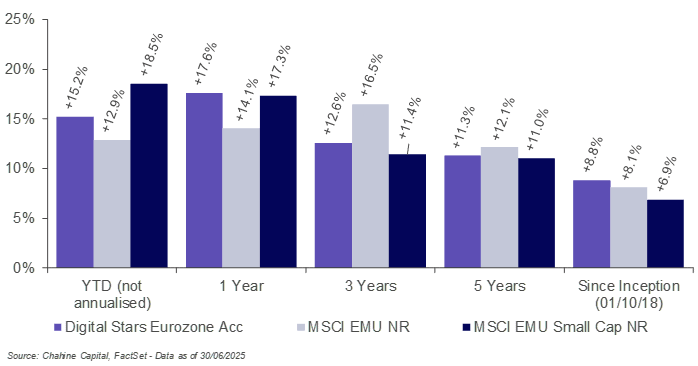

Digital Stars Eurozone (retail share class)

Source: FactSet/Chahine. Data as of 30/06/2025. Past performance is not indicative of future returns.

Digital Stars Eurozone benefited from a market environment that favoured its “pro-cyclical” all-cap positioning over the half-year. It also benefited from good stock selection and neutral sector positioning. The main contributors were financials and industrials. In terms of the fund’s positioning, the overweight in the financials sector, the main positive contributor to performance, was offset by an overweight in the consumer discretionary sector, particularly luxury goods.

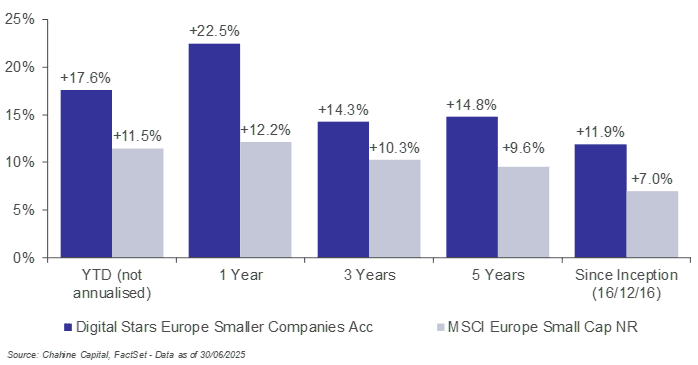

Digital Stars Europe Smaller Companies (retail share class)

Source: FactSet/Chahine. Data as of 30/06/2025. Past performance is not indicative of future returns.

During the first half of the year, Digital Stars Europe Smaller Companies benefited from a good selection of stocks, supported by a positioning that was well aligned with the strongest underlying market trends. Good earnings announcements for the stocks in the portfolio, as well as an overweight in the financial sector and defence stocks, made a positive contribution to outperformance.

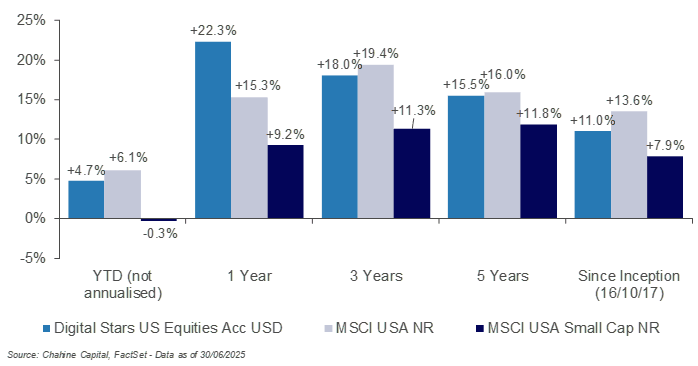

Digital Stars US Equities (retail share class)

Source: FactSet/Chahine. Data as of 30/06/2025. Past performance is not indicative of future returns.

In the first half of 2025, the US equity markets experienced a sharp correction, followed by a rapid rebound on the back of political developments, particularly on the issue of tariffs. This environment has benefited the largest caps, and the index is leading Digital Stars US Equities in terms of year-to-date performance, because of the fund’s all-cap allocation. However, the fund stands clearly ahead of the small cap index, showing the good stock selection of the strategy, particularly in the technology, industrials and consumer discretionary sectors.

FOCUS ON DIGITAL STARS EUROPE

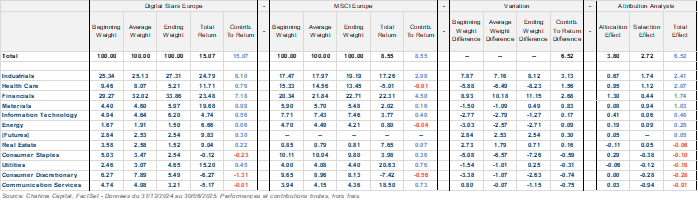

Over the first half of 2025, Digital Stars Europe’s “pro-cyclical” all-cap positioning has been buoyant, particularly since the beginning of March. After a difficult start to the year in relative terms for small and mid caps, which have been well represented in the portfolio, these recovered from March onwards, benefiting the fund’s truly all-caps positioning. The new situation in transatlantic relations has certainly contributed to this turnaround, pushing the theme of sovereignty in different ways. In terms of economic sovereignty, since European small and mid caps are less dependent on trade with the United States, the context has been more favourable for them than for the larger, more globalised companies. As for military sovereignty, this was reflected in the market’s renewed appetite for defence-related companies, which are also well represented in the fund, particularly in the industrial sector (Kongsberg Gruppen, Rheinmetall, MilDef, etc.). The value theme continued to build on its momentum of 2024, while remaining well represented in the fund over the half-year, particularly in the banking (BPER, Banco de Sabadell) and insurance (Unipol Assicurazzioni) sectors. M&A rumours and manoeuvres in the Italian financial sector provided additional support for the sector. In addition to its overweight positions in financials and industrials (two of the market’s leading sectors in terms of weight and performance), the fund also benefited from excellent sector positioning through its marked underweight in healthcare and consumer staples.

Digital Stars Europe performance attribution vs. MSCI Europe, by GICS sectors

Gross performance and contribution, excluding fees. Data as of 31/12/2024 to 30/06/2025. Past performance is not indicative of future returns.

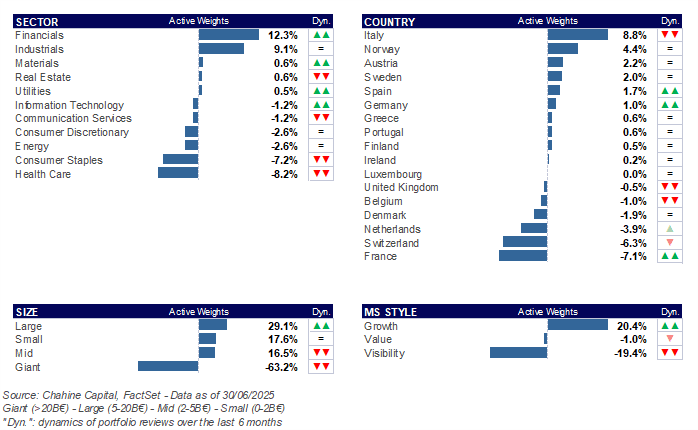

Portfolio dynamics

Positioning of Digital Stars Europe vs. MSCI Europe as of 30/06/2025.

These breakdowns evolutions are not constant and may change over time.

The portfolio’s style profile remained relatively stable over the first half of the year. In relative terms, the quality/visibility style generally behaves in the opposite way to the value style. Consequently, being underweight “quality/visibility” allowed the fund to be positively sensitive to the value trend that dominated the market in the first six months. The theme of the revaluation of value assets continued over the half-year, and should continue for certain segments that are still priced at a discount.

In terms of sectors, this stylistic positioning continues to translate into a clear overweighting of the financials and industrials sectors, and an underweighting of healthcare (especially pharmaceuticals) and consumer staples. This sector allocation remained stable over the period.

In geographical respects, Italy still represents the fund’s largest overweight, although this has been reduced in recent portfolio reviews. France remains the most underweight country.

Finally, our economic momentum indicator continues to show that the Eurozone economy is in a positive dynamic. This pro-cyclical regime is a priori more favourable to small caps in relative terms. The fund has therefore continued to apply an equal-weight logic for new entrants during portfolio reviews. As a result, the fund has an appropriate allocation that boosts exposure to small and mid caps and underweights the largest market caps. Our indicator could switch to contracyclical mode in the second half of the year. This would have the effect of reducing the underweight in the giant caps, as remaining too underweight in this market segment would represent a major active risk in this type of macroeconomic context.

Strong stylistic, sectoral and geographical trends benefited the Momentum factor as implemented in the European Digital Stars strategies, which significantly outperformed over the year. We will now attempt to analyse the forces that we believe will determine the performance of the European and US equity markets in the second half of the year.

Fundamental normalization led equity markets in the first half of the year

The stock market rally that began almost 3 years ago continued during the first half of the year (MSCI Europe NR +8.5% in Euro, MSCI USA NR +6.1% in USD), despite the particularly dense political and geopolitical news.

However, not all segments of the equity market benefited from this rise, and performance was atypically widely dispersed.

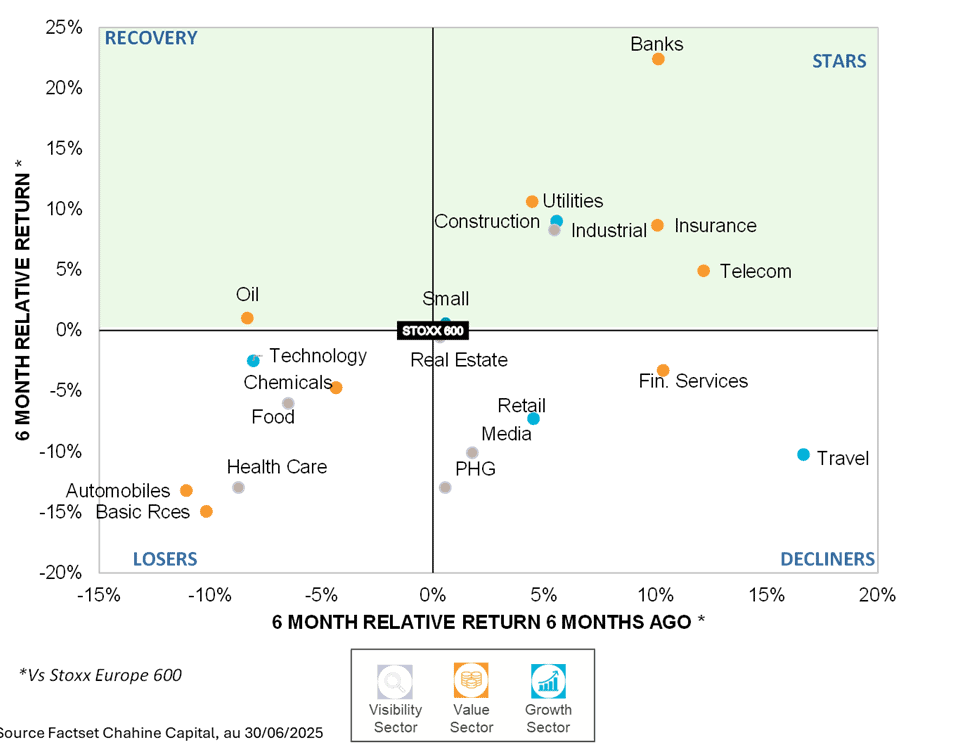

In Europe, for example, the banking sector gained +29.1% in the first half, while the consumer goods and healthcare sectors both lost -6.3%.

Source: FactSet/Chahine Capital. Data as of 30/06/2025.

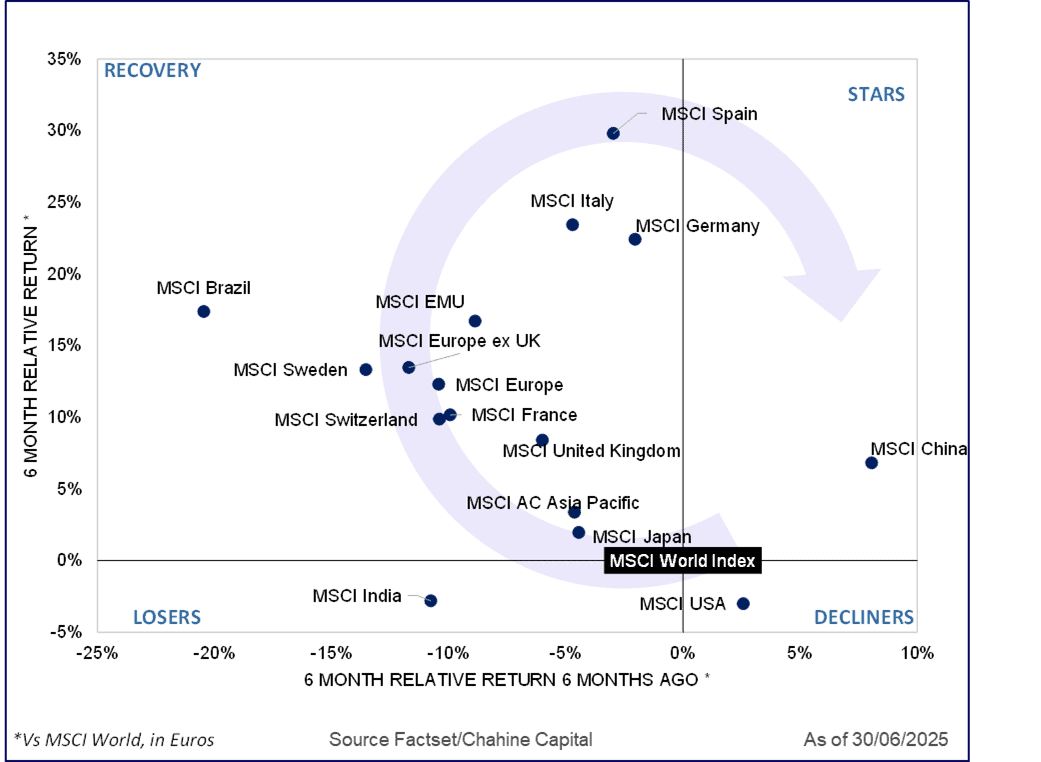

Geographically, the US Dollar decline (-13.3% vs. Euro) was such that, expressed in Euro, US equities declined by -5.9% strongly underperforming Europe and China in the first half of the year.

Source: FactSet/Chahine Capital. Data as of 30/06/2025.

A perfectly intelligible and logical phenomenon in what could be the third and final stage of the stock market rally initiated in autumn 2022.

The first stage, between September 2022 and October 2023, was seen as easing up on the economic cycle. The global economy was proving far more resilient than anticipated, despite inflation at the time running into two digits.

The second stage, between October 2023 and December 2024, was the positive consequence of rapidly falling inflation and the imminence of an accommodating monetary pivot by central banks, which materialized in June 2024 for the ECB and September 2024 for the Fed.

The third phase, which has taken root since the beginning of the year, is that of the fundamental normalization of the various equity market segments. This phenomenon is traditionally observed at the end of an expansionary cycle.

Fundamental normalization boosted Value

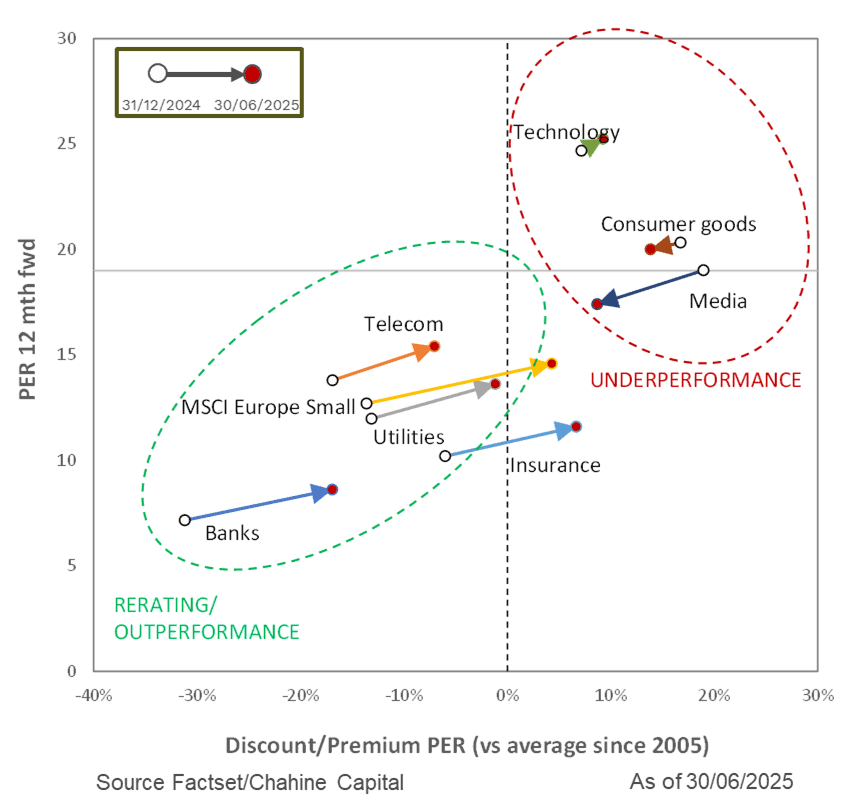

This fundamental normalization explains the good performance of the Value segment and of small and mid-cap compartment in Europe during the first half of the year.

At the start of the year, all Value sectors, i.e. those with low valuations, were at a discount to their historical valuation standards. This is no longer the case. Conversely, the “expensive” sectors, notably the Visibility sectors (Food, Consumer Goods, Health Care, Media), exhibited a valuation premium at the start of the year, which their recent significant underperformance has gradually helped to normalize.

Source: FactSet/Chahine Capital. Data as of 30/06/2025.

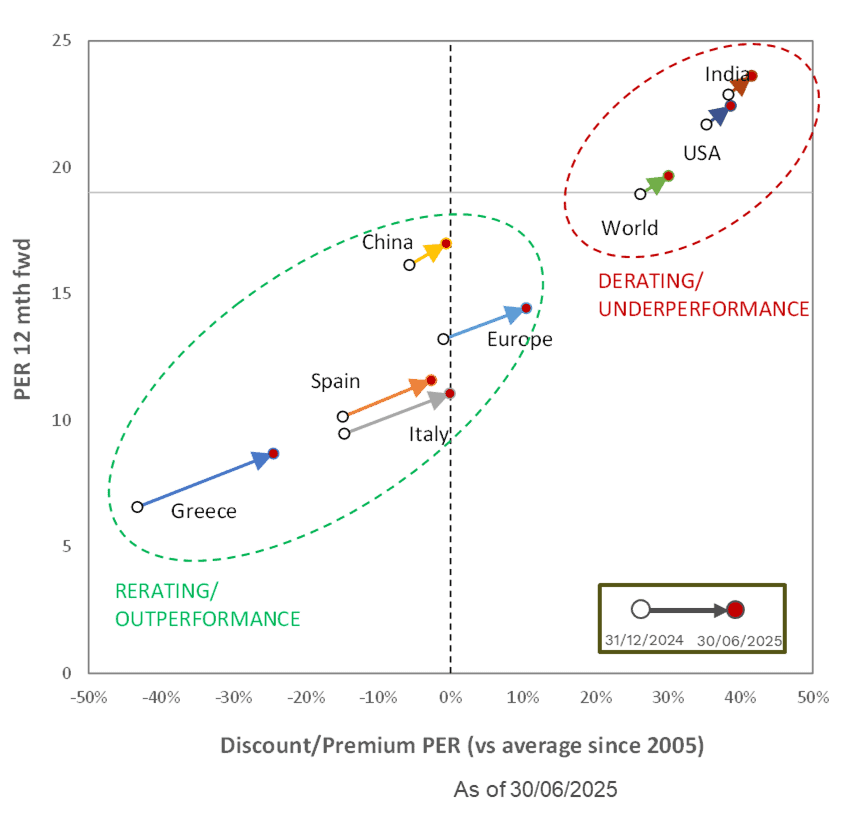

The behaviour of the various geographies also contributes to this phenomenon of fundamental normalization. Europe’s strong outperformance is gradually reducing the historical discount observed at the start of the year. At the same time, the opposite phenomenon was observed in India and the United States during the half-year.

Source: FactSet/Chahine Capital. Data as of 30/06/2025.

Rising euro and trade tariff soap opera lift Europe’s domestic segments

This fundamental normalization in the first half of the year also lifted Europe’s most domestic market segments. This will surprise no one in a political context dominated by the new Trump administration’s threats of tariffs. All the more so as the euro rose sharply against the dollar, weighing on exporting companies in relative terms.

Banks, Insurance, Telecoms and Utilities stood out, as these sectors combine Value and domestic characteristics, unlike Consumer Goods, Healthcare or Automobiles.

This phenomenon also supported small and mid-cap stocks in relative terms. The latter generate only 13% of their sales in the United States, compared with 25% for large caps on average.

A more diversified Momentum in the second half?

The normalization process has been such that the fundamental discrepancies have now largely been rectified.

It would therefore not be surprising to see a gradual shift in the Momentum, which is currently highly polarized, towards segments that have been neglected.

Indeed, some segments have underperformed to such an extent that they are once again becoming attractive. In Europe, Food & Beverage, Healthcare, Consumer Goods, Luxury Goods and Automotive are all part of this trend. In the United States, a stabilization, or even a retracement, of the US dollar could boost small and mid-cap stocks in relative terms, which were neglected in the first half of the year.

The catalyst for this could be a larger-than-expected rate cut by the US Fed in the second half of the year, which would enable the Trump Administration to loosen its grip on tariffs and restore the confidence of investors scalded by the isolationist tendencies of the first half of the year.